The Central Bank’s international reserves, one of the weak points of current economic policy, are the subject of constant monitoring by investors and analysts.

Within this accounting, special attention is paid to the so-called “net international reserves” (RIN), whose goal the government and the IMF have already agreed to reduce, from the USD 2.4 billion initially stipulated to – USD 2.6 billion in the first review of the agreement signed in April.

That is, the Fund has already “forgave” Economía a margin of USD 5,000 million and there are consulting firms, such as Equilibra, that estimate that the government is today between USD 7,000 and 8,000 million below the revised goal.

A new analysis, from the consulting firm PxQ, which heads Emanuel Álvarez Agiswho was vice minister of Economy during the administration of Axel Kicillof At the head of the portfolio, he also calculated that if the USD 14,000 million that the IMF has already disbursed are subtracted from the current reserves, the net reserves are at a similar level, and even slightly lower, than that of November 2023, on the eve of the presidential inauguration of Javier Milei.

According to PxQ, the reserves were then negative at USD 11,133 million, and if what the Fund sent since last April is subtracted, they are now negative at USD 11,482 million.

Under the April agreement, the Fund made an initial disbursement of USD 12,000 million to “clean up” the BCRA’s liabilities, which the Treasury assumed, and another of USD 2,000 million.

The debt with the IMF is from the Treasury, not from the BCRA, but in the event of maturities in dollars, if it is not able to refinance them, the Treasury will have to pay by selling pesos from the fiscal surplus that it accumulated and deposited in the Central Bank, for close to USD 10,000 million. Beyond the accounting equivalence, the monetary entity has the real dollars.

Hence the PxQ calculation and also the criticism of several analysts of the economic team for not having bought dollars “within the exchange band”, as suggested by the agreement with the IMF, between mid-April and June, a period of greatest agro-export liquidation, when the currency was trading at between $1,100 and 1,300 and the government (including President Milei) decided that it would not buy dollars unless the price was at the “floor” of the band. initially at $1,000 and falling at 1% monthly.

Last Sunday, interviewed by LN +, when the question was raised, Minister Caputo responded: “this is the Government that bought the most dollars in history, in 20 months we bought USD 29,000 million (…) we could not keep most of those reserves because we have had to cancel debt.” The previous Government – he explained – “made a restructuring such that the capital cancellation fee did not fall into their government but into ours.”

The explanation diluted the questioned praxis in a broader period: that the Government refrained from buying dollars when it was between $1,100 and 1,300 and then bought much more expensively, to prevent the price from piercing the ceiling of the band. He even paid a high fiscal price by temporarily eliminating withholdings to obtain dollars.

Then he received help from the US Treasury, which bought pesos and sold dollars while announcing a future “currency exchange” for USD 20,000 million, an amount that the head of the Treasury later Scott Bessentgrew to a potential of USD 40,000 million via official and private sources.

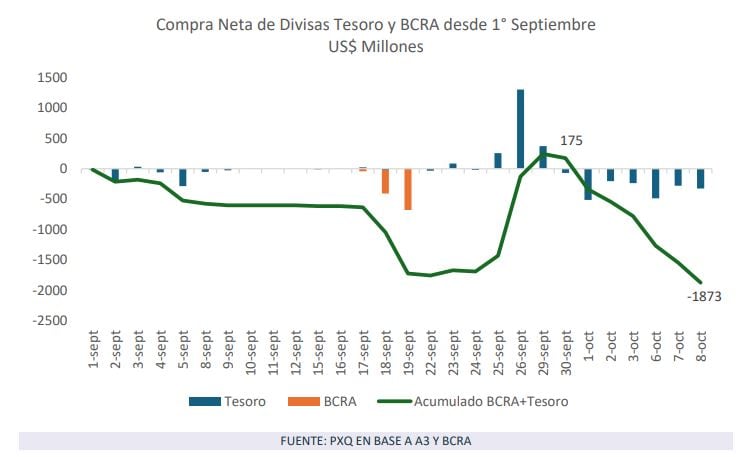

PxQ shows that from September 1 to October 8 the government made net dollar sales of USD 1,873 million. “The macro program and its different phases have already exhausted the positive effects of two bailouts: the money laundering and that of the IMF. And in a short time, the shock on the expectations generated by Bessent’s publication was also exhausted. After buying US$ 2,000 million as a result of the extraordinary liquidation of the oilseed-cereal complex due to the temporary elimination of withholdings, the Treasury sold US$ 2,100 million in the following 7 wheels to defend an exchange rate parity in the area of $1,425-1,430 (per dollar),” he says in this regard.

“Treasury deposits stood at USD 342 million on October 9; it did not have much firepower left to prevent the official exchange rate from reaching the upper limit (…). At the ceiling of the band, the one selling is the BCRA, which already had its interventions between September 17 and 19, when it sold US$ 1.1 billion,” the report recapitulates the exchange rate fluctuations of the last month and a half.

According to the same analysis, the main challenge for the Economy in 2026 is how to face debt maturities without access to the market. The report specifies that capital commitments with private creditors total USD 5.7 billion and that after Milei’s first meeting with Trump, Bessent said that “after the election” on October 26, work will be done on this issue, and that after the second meeting Milei-Trump anticipated that in addition to the currency swap for USD 20 billion, they are working on a line of credit for another USD 20 billion.

Regarding what this help could be like if Milei wins the PxQ election, he outlines three possibilities:

1-The US Treasury as guarantor. For which a debt exchange should be carried out. “Argentina would offer creditors new instruments whose payment would be guaranteed by US Treasury securities,” he hypothesizes, and compares this potential operation with the Brady Plan of the late 1980s.

2-Loan to cover payments. The BCRA would arrange a REPO with banks guaranteed by the US Treasury. “Then the BCRA would sell the dollars to the Treasury to cover payments to private creditors. This alternative would be easier to implement, given that it would not require an exchange process or go through Congress to become effective,” says PxQ.

3-Scott’s promise. A third option, taking Bessent’s phrase of doing “whatever is needed”, would be a program to buy back Argentine securities in the secondary market by the US Treasury, similar to what the European Central Bank (ECB) did in 2012 to help countries like Greece, Portugal and defend the euro. In that case, the announcement by the then head of the ECB, Mario Draghi, “It was of such magnitude that intervention did not even have to be carried out in the secondary market for public securities.” This credibility effect has not been achieved until now, despite the repeated political promises of the Trump government and the concrete interventions of the US Treasury.

The PxQ report makes an analogy between the concerted intervention of the US and its G7 partners in 1985, in the so-called “Plaza Agreement” (after the Hotel in which it took place) to end the overvaluation of the then so-called “super-dollar” and boost the appreciation of the Japanese yen and the German mark.

There was, says the consultancy, an alignment of interests and concerted actions: it was the time when the US feared that Japan would “buy” New York and figures like the then CEO of Chrysler, Lee Iaccocawarned about the death of North American automakers at the hands of the Japanese.

“The agreement was so successful that it led to one of the worst speculative bubbles in history. Japan expanded hand in hand with currency appreciation between 1986 and 1991, inflating the prices of its assets, particularly that of real estate (…) by 1990 property prices had multiplied by four,” says PxQ.

Another successful intervention, through the US Exchange Stabilization Fund, was the “rescue” of Mexico in 1995, during the government of Bill Clintonanalyzed as a contrast to the current Argentine case by Paul Krugmanhypercritical of donald trump and the “help” it is giving to Argentina.

That aid was justified, because Mexico was the destination of 10% of North American exports and is a neighbor whose stability is in the interest of the United States. This is not, says Krugman, the case of Argentina, which absorbs only 0.5% of US foreign sales and is geographically remote.

However, the most pointed aspect of the 2008 Nobel Prize in Economics criticism is that that aid was useful, because Mexico had already devalued and had a “realistic and responsible” government and economic policy. On the other hand, he maintains, Argentina has an overvalued peso that at some point will collapse.

According to Krugman, this would happen sooner rather than later because – he argues – by declaring that aid will only be maintained if Milei wins the elections, “Trump has galvanized the opposition, leading to more capital flight and sky-high interest rates.” And all, he concludes, to help a right-wing government and some millionaires who bought Argentine bonds.